Businesses today are navigating rapid transformations. As new technologies emerge at unprecedented speeds and markets shift dynamically, customer expectations are simultaneously evolving to match this pace. Agility and innovation matter more than ever. In this climate, firms need to track different metrics. Metrics that look ahead rather than behind.

But old accounting methods lag, they worked well once but no longer suffice. Traditional accounting is rear-view focused. It cannot gauge today’s key success factors well enough. Success today depends on innovation, agility, customer centricity, and technology adoption. Traditional accounting measures do not capture these facets adequately.

Innovation accounting fills this crucial gap. It focuses on leading indicators tied to future growth, rather than just retrospective financial data. Innovation accounting makes research and development(R&D) and innovation measurable with relevant metrics. It tracks progress on new products, intellectual property(IP), prototypes, and tech platforms. These lead indicators complement lagging financial results.

This article shows how new and old accounting are different and why it matters. It aims to help accounting professionals use the best of both approaches.

The Emergence of Innovation Accounting

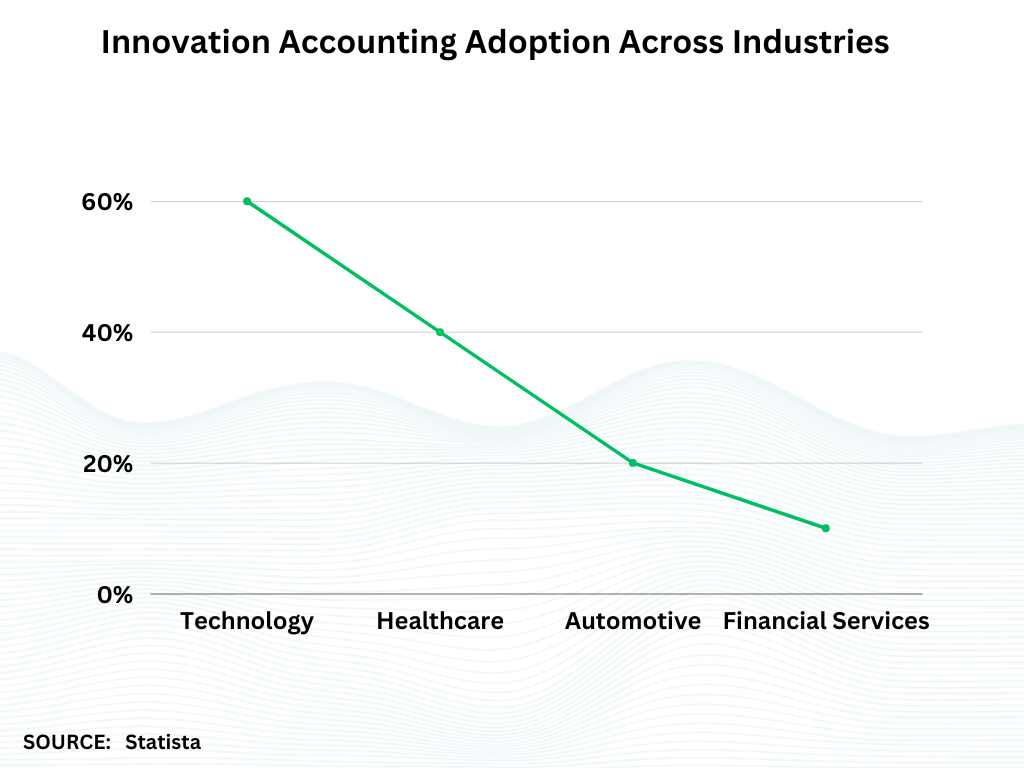

Digital technologies and startups have fueled the rise of innovative accounting solutions. Traditional accounting falls short in fast tech change and iterative product building.

- CB Insights data shows that 9 in 10 startups fail.

- 42% cite no market need for their product.

- This highlights the need to assess market fit well. And gauge innovation viability beyond accounting.

Core Distinctions Between the Two Approaches

Accounting has two distinct branches now – traditional and innovation. Each serves a specific purpose. Their approaches differ. Let’s explore the key divergences.

Basis of Measurement

- Traditional accounting focuses on tangible assets and clear financial numbers. Easy to quantify but limited.

- US Chamber data shows over 80% of firm value is now intangible assets. Things like IP, brand equity, and talent. Harder to measure but crucial.

- Innovation accounting instead emphasizes future potential. And iterative learning abilities, plus adaptability, and the keys to growth now.

- McKinsey notes forward-looking indicators better predict startup success, rather than past finances. Feedback outpaces monetary returns.

Value Proposition

- Traditional accounting uses past data to inform future moves. A rearview approach.

- A KPMG survey found that 90% of firms still rely on past performance.

- As the main metric that guides strategy. But past success does not guarantee future gains.

- Innovation accounting uses present metrics tied to future growth and adaptation of opportunities.

Per Deloitte, over 50% of companies now rank innovation metrics as very important. To forecast growth via current innovation work. Real-time data matters more.

Risk Assessment

Based on traditional accounting assesses risk and current finances.

However, Harvard Business Review notes relying on past data can make firms miss disruptive external opportunities or threats.

Since 2000, 52% of Fortune 500 firms have disappeared. Due to a lack of adaptability, change is now constant.

Innovation accounting considers potential pitfalls too. In innovation cycles and market shifts, plus technology trends. It balances external and internal risk views.

Per Accenture, 93% of executives believe innovations will disrupt their industry. Showing the need to account for innovation risks beyond past financials.

Time Horizons

- Traditional accounting has a short to medium-term focus. With periodic reporting, a quick returns mindset.

- But an EY report reveals 73% of investors now want non-financial disclosures too, not short-term financial reports. Thus, the tide has turned.

- Innovation accounting has a long-term outlook. It considers evolving business models and offerings, playing the long game.

- A PwC study shows long-term focused firms outperform peers in revenue, earnings, jobs, and stock price which is Good for all stakeholders.

- By covering key divergences in-depth, accounting professionals can make informed choices. Blend traditional and innovative accounting for ideal results.

The Critical Significance of Innovation Accounting Now

- Over three years, BCG data shows firms focusing on innovation metrics. Thus shareholder returns are 2.6x higher than the market average.

- This illustrates the tangible payoff of tracking innovation progress, beyond financial indicators.

- Innovation accounting helps firms stay ahead of change. It builds an innovation culture and enables sustained growth. It ensures returns on innovation investments, by making innovation work measurable.

Challenges and Skepticism Faced

Innovation accounting has merits. Now it has with all new concepts, some skepticism exists. Let’s explore the main concerns raised, and how firms can address them.

Subjectivity and Manipulation Risks

- Some see innovation accounting as subjective. Unlike the clear figures from traditional accounting.

- Metrics like brand equity and customer loyalty are qualitative. Numbers can vary based on the calculations used.

- There is a risk of data manipulation too. To inflate innovation successes on paper when real progress is lacking.

- However, firms can ensure authenticity via rigorous protocols and independent third-party audits. Metrics should link to return on investment.

- This quantifies innovation progress in financial terms. Robust systems can cut subjectivity and manipulation risks.

Difficulty Standardizing Metrics

- Innovation types vary across industries. Software and biotech inventions differ as do timelines and costs. This diversity makes standardizing metrics hard.

- However, firms can identify metrics tailored to their innovation workflow. Common indicators include speed to prototype, development costs, and market testing results.

- Tracking the right metrics for one’s industry improves standardization. Industry bodies can issue guidance too.

- To help firms benchmark against peers. The framework will evolve with time and collaboration.

Resistance From Traditional Accountants

Most accountants are trained in traditional methods. Where innovation accounting contrasts the status quo. Adopting it requires an open mindset and re-skilling. When people get used to setting ways, change meets resistance.

Discomfort with new methods can breed skepticism. But the business context has changed. Accounting must evolve along with it, where teaching the next generation both approaches will ease resistance. Emphasizing how innovation accounting complements rather than replaces traditional methods helps too.

Increased Accountability on Innovation Teams

- Innovation accounting makes R&D and innovation measurable. It ties funding to progress and results. This can increase pressure on innovators.

- But some constructive accountability boosts output. It steers time and money to high-potential projects. Companies must ensure teams have the tools and support needed.

- And recognize failures from well-planned experiments. A balance of accountability and autonomy sustains innovation.

- Performance metrics should factor this in and focus beyond financial returns.

Striking the Right Balance

- For success, firms must blend old and new accounting well. Over-indexing on past data creates risk.

- But overplaying innovation metrics can be impractical too. The right balance depends on one’s industry and strategy.

- But a mix of backward and forward-looking indicators works best. Tradition and innovation play key roles in accounting’s evolution.

Best of Both Worlds: An Integrated Approach

- Firms can blend both accounting approaches for a comprehensive financial view.

- Some companies already combine both methods well to leverage the best of both.

Real-World Examples

- Apple uses future-focused metrics like product pipeline health alongside past sales data.

- Amazon tracks quick wins and the cost of innovation along with standard financials.

- Google uses OKRs to make innovation measurable along with traditional accounting.

Blending Both Approaches: Guidance for Accountants

- Use traditional accounting for backward-looking data and to meet compliance needs.

- Apply innovation accounting to make R&D and innovation measurable.

- And to estimate future potential. Learn from peers at innovator companies who have succeeded at this integration.

Key Takeaways

- Innovation accounting is now crucial for sustained performance. As disruption accelerates.

- But it should complement rather than replace traditional accounting.

- Accountants must champion this change within their firms. To drive long-term prosperity. By embracing innovative accounting, accountants can enable business success today and future-proof their relevance as the profession transforms.

FAQs

- Ensuring Reliable Innovation Accounting Metrics?

Rigorous protocols, third-party audits, and refinements help as does tying metrics to ROI.

- Is innovation just a Buzzword or is it genuinely Impactful?

The successes of innovating firms prove it is not just a buzzword. Those who missed out illustrate the costs. Measuring innovation boosts longevity. Rather than leaving it to chance.

- Adopting Innovation Accounting: Tips for Accountants?

Training, certification courses, and an open mindset help drive adoption. Start small by supplementing current methods. Then shift focus to leading indicators.